This should only be used if all other sources of money have been exhausted

Amount to target for emergency fund

6 months to 2 years of living costs

Living costs should include each and every expense that happens, including subscriptions, club memberships, etc

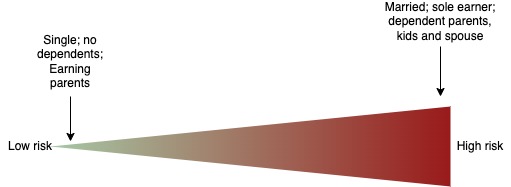

Lower the risk to the household, lower the amount we need to save

If you are the sole earner of the family, and you have non-earning dependents (including kids and parents), then you are at high risk

Where to keep the emergency fund

Best and safest product is fixed deposit

Try to get hold of flexi-FDs that allow you to sweep out a part of the total deposited amount. This will allow you to withdraw just the amount you need, rather than breaking the entire deposit.

Alternative option - short term debt funds

If you are familiar with mutual funds, then you can also park the emergency fund in a short term debt fund.

Choose a conservative fund, not aggressive

Don’t buy a product based on just high returns

Ensure that the top holding of the debt fund is in AAA-rated bonds